SSA has recently redesigned its statements to show benefit estimates at each age from 62 (or the client’s current age if over 62) through age 70. For clients born in 1955 through 1959, whose FRAs are 66 plus some number of months, the statement shows the estimate for FRA (e.g., 66 and 6 months) as well as age 67. In a few (not all) of the cases that we’ve seen, these amounts are the same. Clearly, they should not be. Each month a client delays application, the benefit amount goes up by a few dollars. (See references at the end for the exact formula.)

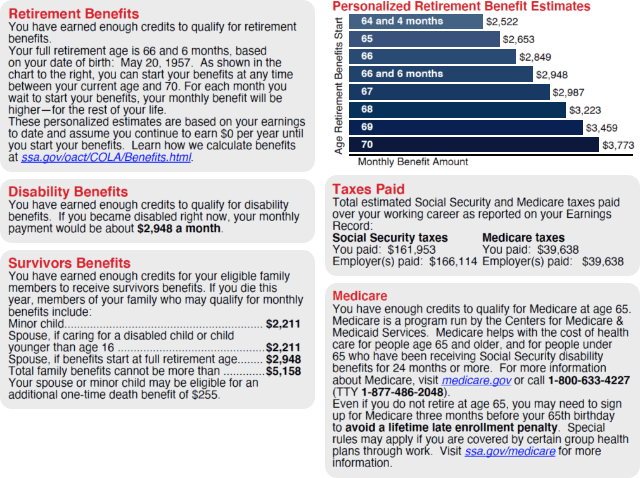

In addition to this error, we are seeing mistakes in the DRCs (delayed retirement credits) between FRA and age 70. For example, one statement showed a benefit of $3,223 at 68, $3,459 at 69, and $3,773 at 70. Instead of going up by 8% a year, the benefit went up by 7.3% between 68 and 69 and 9.1% between 69 and 70.

There have always been some discrepancies between our Savvy calculator numbers and SSA’s estimates (for reasons discussed below), and now these discrepancies may be even wider due to inaccuracies on the Social Security statements. So it will be very important for Savvy advisors to do three things: 1) Be as accurate as possible when entering a client’s PIA into the calculator; 2) Issue a (stronger) caveat that the numbers shown by the calculator will not match the numbers on the client’s Social Security statement—and that the only truly accurate amounts are the amounts the client receives after filing for benefits; and 3) Rerun the analysis each year using the PIA off the client’s latest statement.

If you are taking the PIA off one of the newly redesigned statements, use the estimate for FRA. For clients born between 1955 and 1959, this will be 66 and 2, 4, 6, 8, or 10 months. Confirm that this amount matches the disability estimate in the box where it says, “If you became disabled right now, your monthly payment would be about $_____.” The disability estimate is the client’s PIA. That’s the number to use in the calculator. The calculator will then adjust for claiming age (based on the POMS references at the end of this article) and COLAs.

Other reasons for discrepancies in the numbers

There have always been some discrepancies between our numbers and SSA’s. These come down to COLAs and earnings.

1. COLAs. The estimates on the Social Security statement are in today’s dollars. If you entered a % COLA amount in the calculator (or went with the default 2% COLA), the calculator numbers are shown in future dollars. If you want to more closely match SSA’s estimates, change the COLA to 0%.

2. Earnings. SSA’s estimates assume the client will continue working at the same pay until claiming age. The new statement tells what earnings they are assuming, based on the client’s recent earnings. So the age-62 estimate assumes the client will stop working at 62. The age-70 estimate assumes the client will work to age 70. The FRA-estimate—the PIA—assumes continued earnings to FRA. So if the client stops working before FRA, the calculator will overestimate the PIA. This discrepancy is at its largest when the client stops working before FRA and claims at 70: SSA’s age-70 estimate will be higher than the calculator numbers because it assumes continued earnings to age 70. To increase the accuracy of the PIA when a client will stop working before FRA, send them to the SSA Retirement Estimator. Have them enter a retirement date that coincides with their FRA. This is so the Estimator will give the PIA and not adjust for early claiming. Next, have them enter zero earnings going forward. The Estimator will provide a revised estimate based on the client’s actual earnings rather than one based on the presumption that earnings will continue at the same rate until claiming age. For clients who plan to work to 70 and claim at 70, the calculator numbers will be slightly underestimated (because the PIA presumes earnings to FRA), but I see no need to adjust; let the higher actual benefit amount come as a pleasant surprise when the client claims.

Remember, the purpose of the calculators is to help clients analyze claiming strategies. They are not designed to show an accurate representation of the client’s income stream. Even if the numbers are off a bit, the calculators can be extremely valuable in helping clients understand the lifetime impact of the various claiming options.

Reference

Sample statement