Most people have to wait until the annual Social Security Trustees Report is issued—sometime between May and August—to find out how the OASDI trust fund performed the prior year. But if you know where to look (and we do), you can find out as early as March.

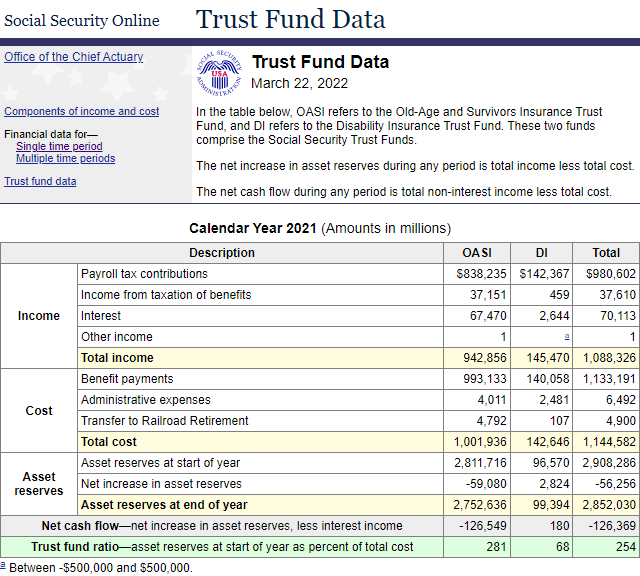

If you go to Financial Data for a Selected Time Period and enter the time period you want—calendar year 2021 in this case—you can see how much the trust fund took in, how much it paid out, and the change in asset reserves at the end of the year compared to the start.

Going right to the bottom line, we see that the trust fund ended the year with $2.852 trillion in assets, or $56 billion less than the $2.908 trillion that it started with. For several years now the trustees have been projecting that 2021 was the year the drawdown would start—that for the first time total costs would exceed income from all sources. (Over the past few years the trust fund has paid out more than it took in in payroll taxes, but interest income and income taxes paid on benefits, which are allocated to the trust fund, kept the trust fund running in the black.)

We bring you this news so you can stay informed and be prepared for the scary headlines that will undoubtedly be written when the trustees report is released—not so you can rush out and warn your clients that Social Security is about to go broke. As the news comes out, there are four things to keep in mind when talking to clients:

- This drawdown was not unexpected; it’s just the beginning of a long, slow drawdown that will eventually exhaust the assets in the trust fund around the year 2034 if Congress doesn’t act. It’s pretty much right on schedule.Congress has been ignoring the warnings, but maybe this report will finally get them to pass the necessary legislation. And remember, payroll taxes will still be coming in. It’s not as if the whole system will be bankrupt.

- There is already legislation in Congress, Social Security 2100 Act: A Sacred Trust, that would begin to address the solvency issue. (This legislation would not restore full solvency because of Biden’s promise not to raise taxes on anyone making less than $400,000 a year; but at least it’s a start and can be revisited when the key solvency provisions sunset in 2027.)

- Whether Congress adopts this or different legislation, benefits for people over 60 are not likely to be affected. We do not expect to see a sudden 22% drop in benefits across the board in 2034. Rather, we would look for legislation that would phase in a gradual increase in payroll taxes as well as a gradual lessening in the escalation of benefits for future retirees.

- If pre-retirees want to be ultra-conservative and either not count on Social Security at all or make it a smaller component in their retirement income mix, they can certainly take it upon themselves to beef up their own retirement savings.

We will get more information on the factors that went into the trust fund’s 2021 results as well as the trustees’ revised projections when the annual report comes out. Start watching for it in May.